1H24 Web3 Fundraising

Early-stage fundraising review: pre-seed to Series A in 1Q24 and 2Q24

Summary

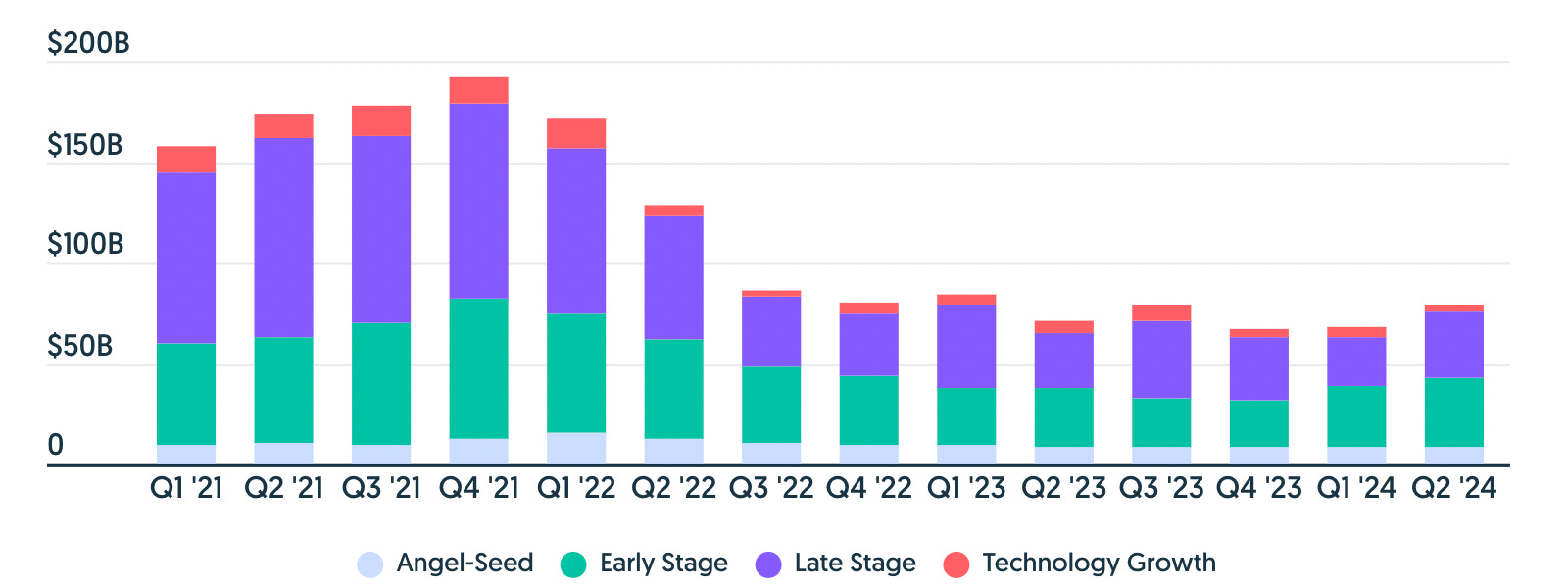

In 1H24, Web3 fundraising saw a notable increase, with $7.52 billion raised across 1,240 projects—a 24% rise in capital and a 58% increase in deal count compared to 2H23. This outpaced the broader VC market, which saw a 16.1% rise in capital but a 16.7% drop in deal count.

Pre-seed stage fundraising in Web3 has been resilient, with 1H24 setting a new record for capital raised at this stage ($189 million across 80 deals). Series A fundraising also showed strong growth, with $1.56 billion raised across 77 deals, nearly double that of 2H23.

The global startup funding environment improved in Q2 2024, driven by mega-rounds and a surge in AI funding, which doubled to $24 billion. Despite fluctuations, the overall market has seen a gradual recovery, particularly in seed and Series A stages.

The increase in AI and Web3 investments suggests strong investor confidence in these high-growth sectors, contributing to a more stable and improved market environment in 2024. This trend indicates potential upward momentum in the coming quarters, particularly in early-stage deals.

1H24 Highlights

In 1H24, $7.52bn was raised across 1240 projects across all stages. This represents a 24% increase in the capital fundraised and a 58% in the number of deals from 2H23.

$3.66bn was raised by 624 projects in 1Q24, down 6.2% in capital fundraised from the previous quarter.

$3.86bn was raised by 616 projects across all funding stages in 2Q24, up 5.5% in capital fundraised from the previous quarter.

Upon initial inspection, 1H24 has not performed as well as 1H23: $13.9bn in capital raised from a deal count of 1041. This means that there was 45.8% less capital raised in 1H24 when compared to 1H23.

The significant difference, however, can be explained by a single success story of one company. In March 2023, Stripe raised $6.5bn. This alone accounted for 83% of the capital raised that month. It also accounted for 63% of the capital raised in1Q23 and 47% of the 1H23 total. If we treat Stripe’s fundraise as an anomaly and remove it from the dataset, then 1H24’s performance was 2% greater in capital fundraised than the first half of last year: $7.36bn raised in 1H23 with Stripe removed.

Looking at the wider VC market, $39.6bn was raised across 2525 deals in 1H24. By comparison, in 2H23 $34.1bn was raised across 3031 deals. This represents a 16.1% increase in capital fundraised but a 16.7% decrease in deal count from 2H123 to 1H24.

According to Carta, in Q2 2024 the deal count and total capital raised saw significant growth compared to Q1 2024, with 1,287 rounds totalling $20.9bn, marking a steady quarter by quarter improvement from 3Q23. 2Q24 recorded the highest amount of VC cash invested in the past 12 months.

Global startup funding saw an uptick in the second quarter, reaching $79 billion—a 16% increase from the previous quarter and a 12% rise from the $71 billion invested in Q2 2023. Much of this growth was driven by mega-rounds, where investments exceeded $100 million. Crunchbase data indicates that we are currently eight to nine quarters into a broader funding decline. Although this quarter ranks among the highest since Q1 2023, it doesn’t necessarily signal a full recovery in the venture market. Since 2023, funding levels have fluctuated quarterly, largely due to an increase in large growth rounds for pre-IPO companies and those in the AI sector.

Overall, it appears that there has been a marginal improvement in fundraising performance in the Web3 sector compared with the wider VC market. This is not just due to the relative increase in capital raised (+24% in Web3 vs +16% in the wider market) but also due to relative marked increase in Web3 fundraising deals (58% in Web3 vs -17% in the wider market).

Web3 Pre-seed fundraises

Pre-seed stage fundraising has been the most resistant to the bear market trends since 2Q23 when compared to other stages in the Web3 sector and the wider VC market. Since 3Q23, there has also been a quarter on quarter increase in the number of pre-seed deals. 1Q24 also saw the highest amount of capital raised for pre-seed deals in Web3 VC history: $106m raised across 36 deals.

Source: Messari. Web3 pre-seed deals and capital raised per year half. This has also translated into a new all-time high for capital raised in Web3 pre-seed deals in a six month period: $189m raised across 80 deals in 1H24 vs previous high of $184m across 102 deals in 1H22.

Web3 Seed and Series A fundraises

Data from Carta provides context for how the wider VC market for seed and Series A deals are performing. The seed deal count in 2Q24 is nearly on par with 1Q24. Series A deals in 2Q24 outperformed the previous quarter, suggesting that 2Q24 might mark a turning point from 1Q24, which saw the lowest quarterly deal counts for both seed and Series A since early 2019. While total cash raised for both stages increased modestly in 2Q24, it's noteworthy that 1Q24's Series A funding was the lowest in five years. Although 2Q24's 16% increase still places it among the lowest-earning quarters for Series A, it could mark the start of an upward trend. This, however, is a weak indicator.

Within this context of the wider fundraising market, the anticipated upward trend for seed and Series A deals is more pronounced.

In 1H24, $1.23bn was fundraised at seed stage across 256 deals, representing a 47% increase in capital raised and a 49% increase in deal count from the previous year half. There have been two consecutive quarters of deal growth and although there was a downward tick of 7% in seed stage capital fundraised from 1Q24 to 2Q24, the total capital raised in this last quarter is still greater than any one period from 2Q23 to 4Q23.

This upward trend is stronger for Series A Web3 deals, wherein both capital fundraised and deal count has increased per quarter since the end of 4Q23, unlike pre-seed or seed stage deals in the same period. Overall, the $1.56bn raised in 1H24 across 77 Series A deals was almost double that of 2H23 (an increase of 97%) and also represents a 75% in deal volume.

Additionally there has been a surge in AI funding which doubled quarter-over-quarter to $24 billion, which accounted for a substantial portion of the total investment. Public token sales maintained dominance, while early-stage venture activity remained stable, suggesting that investor confidence in high-growth sectors like AI and Web3 remained strong, helping to stabilise and improve the market environment in 2024.

For monthly snapshots of the Web3 fundraising market, please see 0xCheekyRolo.

For more token-specific insights, please see Jasper de Maere, ‘Token Trendlines #1 – Fundraising Deep Dive’, August 2024, Outlier Ventures.